The retail trading sector has experienced structural shifts, yet the underlying market data remains remarkably consistent. Quantitative industry audits indicate that the retail trading survival rate remains low, with approximately 90% of individual accounts failing to sustain profitability over a multi-year horizon. This persistent failure rate is rarely caused by poor technical indicators or inaccurate market forecasting models. Instead, institutional analyses demonstrate that sustainable market longevity is governed by a precise combination of mathematical metrics and behavioral systems.

This extensive breakdown explores the foundational successful trading factors that dictate long-term portfolio growth. By examining structural capital constraints, statistical probability distributions, and cognitive risk frameworks, you will discover how to transition from reactive retail behavior to an institutional-grade methodology.

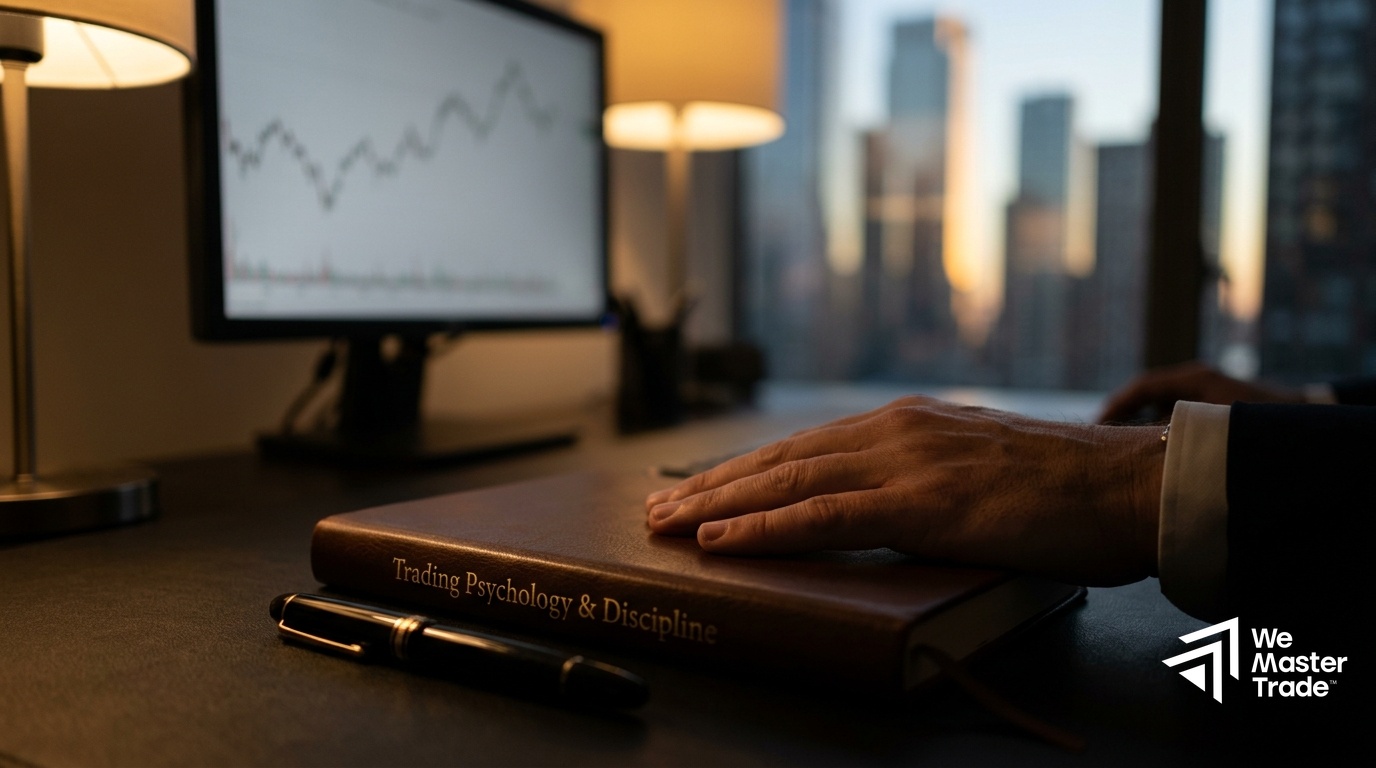

The Psychological Framework of Consistently Profitable Traders

Market execution is fundamentally an exercise in managing cognitive bias under conditions of absolute uncertainty. While a novice operator seeks external market certainty, a seasoned professional relies on internal behavioral controls to ensure system consistency. The human brain is naturally poorly wired for probabilistic environments, frequently falling prey to prospect theory—the behavioral economic phenomenon where the psychological pain of a financial loss is twice as intense as the pleasure of an equivalent gain.

This innate cognitive bias triggers classic execution failures: cutting profitable positions prematurely out of fear and extending losing positions in the irrational hope of a structural reversal. Developing strict trading psychology principles requires a complete detachment from individual trade outcomes. Professional market operators treat every single trade setup as a lone data point within a vast probability distribution.

To insulate execution from emotional volatility, professional operators install hard technical guardrails. Implementing an automated, rule-based approach allows individuals to trade without stress by eliminating discretionary hesitation during high-volatility market regimes. This process shifts the operator’s focus away from floating account balances and repositions it entirely onto technical execution quality and rule compliance.

Overcoming Behavioral Pitfalls with Quantified Metrics

Uncontrolled psychological responses systematically destroy trading accounts through revenge trading, over-leverage, and random stop-loss adjustments. True professional trading discipline relies on a structured framework where every market action is quantified before capital allocation occurs.

By defining exact technical parameters for entries, target invalidations, and profit taking, you successfully transfer operational control from the emotional limbic system to the logical prefrontal cortex. This structural separation turns market execution into a highly mechanical, repetitive process.

Developing a Mechanical Trading Edge vs. Discretionary Execution

A common misconception among retail market participants is that professional performance requires predictive market forecasting. In reality, a sustainable profitable trading system does not predict future price action; it merely exploits an architectural inefficiency within financial markets to establish a clear statistical edge. This mathematical edge ensures that across a sufficiently large sample size of executions, the cumulative revenue generated from winning setups exceeds the combined capital lost on failing positions.

Establishing this edge requires a rigorous data-driven validation process. When backtesting trading systems, developers must evaluate historical asset classes across highly distinct market regimes, such as high-volatility expansion phases, low-volatility compression structures, and structural trend reversals. Failing to account for changing structural liquidity pools and volatility clustering during historical testing yields fragile systems that experience rapid equity curve degradation when exposed to live market environments.

The table below outlines the core performance metrics required to accurately quantify a statistical edge trading strategy over a minimum baseline sample size of 100 historical trades:

| Metric Category | Formula / Definition | Institutional Benchmark Target |

| System Expectancy | (Win% x AvgWin) – (Loss% x AvgLoss) | Greater than $0.20 per unit risked |

| Profit Factor | Gross Profits / Gross Losses | Minimum 1.50 across all regimes |

| Max Drawdown | Peak-to-trough equity curve decline | Less than 10% structural threshold |

| Win Rate | (Winning Trades / Total Trades) x 100$ | 40% to 60% (highly variable via RRR) |

To prevent arbitrary execution deviations, traders should implement a rigid market analysis methods matrix. This technical protocol dictates that an entry order can only be authorized when multiple independent market variables—such as higher-timeframe order flow alignment, historical liquidity sweeps, and immediate fair value gap mitigations—converge simultaneously.

The Impact of Capitalization Size on Trading Performance

The primary structural bottleneck limiting retail trading success is chronic under-capitalization. When an individual attempts to generate a full-time living wage from a micro equity base, they are mathematically forced to apply excessive leverage or assume unsustainably high risk percentages per trade. This operational environment creates an inescapable feedback loop where minor sequence-of-returns drawdowns quickly result in catastrophic margin liquidation.

Furthermore, a small capital base introduces severe psychological pressure. A 2% drawdown on a small account might represent minimal absolute capital, but the realization that the account cannot generate meaningful yield triggers a shift toward reckless over-trading. Conversely, having access to institutional-scale professional trading capital completely alters the execution dynamic.

When an asset manager or independent operator commands an institutional allocation, they can easily meet their absolute financial return objectives while risking a conservative 0.5% to 1.0% of principal balance per trade setup. This protective insulation from absolute financial stress allows the operator to maintain strict compliance with their position sizing strategy, ensuring that a consecutive string of natural losses never threatens their structural market survival.

Advanced Risk Management: The Mathematics of Longevity

Surviving financial market drawdowns is fundamentally a mathematical challenge, not a technical analysis problem. Professional trading risk management operates on the ironclad principle that capital preservation always takes precedence over profit generation. The speed of equity curve recovery is highly non-linear, as shown by the compounding geometric asymmetric recovery curve:

R = D / (1-D)

Where D represents the percentage drawdown experienced, and R represents the exact recovery return required just to return to the initial equity baseline.

A minor 10% account drawdown requires a straightforward 11.1% recovery return. However, if a trader permits a structural account decline to reach 50%, they are mathematically forced to generate a grueling 100% return on their remaining capital base just to achieve break-even status.

Account Drawdown (%) | Required Return to Break-Even (%)

———————————————————-

10% | 11.1%

25% | 33.3%

50% | 100.0%

75% | 300.0%

To completely eliminate the mathematical probability of ultimate account ruin, professional frameworks implement rigorous algorithmic risk control modules. This system requires setting a mandatory stop-loss placement for every active order, calculated via current market volatility using metrics like the Average True Range (ATR).

Positions must be sized dynamically based on the exact distance between the structural entry price and the technical invalidation point, ensuring that the total risk exposure remains capped at a predefined percentage of net account equity.

Why Standard Evaluation Challenges Fail Most Traders

The rise of the retail proprietary trading industry has expanded access to institutional balances, but traditional business models have introduced structural barriers. Statistical assessments show that fewer than 15% of retail participants successfully navigate traditional multi-phase evaluation protocols. This low success rate is caused by artificial performance restrictions designed to shift the mathematical odds against the individual.

Traditional prop firm evaluations frequently impose strict time limits paired with aggressive profit targets. These restrictive parameters force participants to abandon their core risk mitigation frameworks and adopt highly volatile trading styles during unfavorable market conditions. When an operator is forced to hit an arbitrary 10% profit milestone within a short window, they are systematically pushed toward over-leveraging and violating core risk rules.

Furthermore, these traditional structures frequently exploit trailing drawdown models calculated relative to unrealized high-water mark profits rather than realized account balances. This specific metric structure means that if a trader goes into positive floating equity before a trade reverses into a planned trailing stop, their allowable maximum drawdown limit moves upward, permanently shrinking their total operational safety cushion.

Shifting to an Evaluation-Free Paradigm

Recognizing these structural limitations, modern capital providers have introduced an alternative operational path. By choosing to secure capital via instant funding prop firms, professional operators completely bypass these artificial, rule-heavy evaluation phases. This approach grants immediate access to live capital balances, allowing individuals to execute their proven strategies with a long-term perspective.

Implementing a Professional Trading Infrastructure

Moving from casual retail execution to institutional-grade operations requires a standardized mechanical setup. Traders must treat their daily operations as a systematic business process, utilizing a strict trading plan checklist before executing any position across live financial markets.

A core element of this institutional infrastructure is the maintaining of comprehensive trade logs. A professional trading journal metrics routine should meticulously track multiple key variables for every single transaction, including:

- Precise entry and exit timestamps relative to high-liquidity session windows.

- The exact technical asset class and market regime classification.

- Initial planned risk-to-reward ratio versus the actual realized execution ratio.

- Calculated position sizing strategy parameters and maximum experienced adverse excursion (MAE).

Regularly auditing this quantitative data allows operators to identify deep behavioral inefficiencies, spot structural system decay, and refine execution parameters to ensure long-term drawdown mitigation.

Key Questions About Successful Trading Factors Answered

What is the single most critical factor in trading success?

While technical market analysis matters, mathematical risk management combined with strict execution discipline is the ultimate factor. A trader utilizing a conservative 40% win rate can maintain steady long-term equity growth by maintaining a high risk-to-reward ratio and keeping drawdowns tightly capped.

How does account size impact a trader’s success rate?

Under-capitalization systematically forces retail traders to over-leverage to achieve meaningful financial returns, which triggers emotional decision-making and rapid account ruin. Accessing immediate, institutional-scale capital removes the psychological pressure to force sub-optimal setups.

Why do most traders fail traditional prop firm evaluations?

Traditional evaluations introduce artificial time limits and rigid rules that conflict with natural market cycles, forcing traders to over-trade or take sub-optimal risks to hit arbitrary goals. Removing the evaluation phase entirely allows traders to focus strictly on proper execution.

How does a dedicated risk management team benefit a trader?

A dedicated risk management unit monitors systemic exposure, helps curb behavioral biases like revenge trading, and aligns retail execution with institutional safety standards. Professional copy-trading mechanisms can also scale high-probability setups efficiently.

The WeMasterTrade Advantage: Direct Capital Alignment

Achieving consistent market profitability requires more than technical execution; it demands access to an uncompromised capitalized infrastructure. Founded in 2021 in Canada, WeMasterTrade solves the core problems of retail under-capitalization and restrictive challenge rules by providing immediate capital access to skilled market operators globally.

Through its innovative angel funding model, WeMasterTrade eliminates traditional evaluation roadblocks by offering an instant funded account framework with no challenges, no evaluation periods, and no artificial time limits. This operational layout allows traders to focus on execution consistency, safe capital allocation strategy, and professional drawdown mitigation from day one.

The core differentiator of the WeMasterTrade platform lies in its collaborative structural design. The firm employs a dedicated, institutional-grade risk management team that monitors live portfolios to identify high-probability setups. When verified, these professional positions are copy-traded at an expanded ratio of up to 1:4 alongside the trader’s account, directly linking the firm’s profitability to the individual’s long-term success.

With multiple industry awards won since 2021 and a premier profit split of up to 90% in the trader’s favor, this model represents a true partnership. Traders who want immediate capital access without months of evaluation will find WeMasterTrade’s structure worth examining.